The fallout from the US-Israeli attacks on Iran is pushing oil and gas markets towards a full-blown crisis. In the space of a few days:

- daily oil and gas production has dropped by as much as ten million barrels per day from normal levels.

- the Brent crude oil price benchmark has surged from $60/barrel to over $100 as of the time of writing.

- the International Energy Agency has ordered the largest-ever release of strategic petroleum reserves to relieve some of the pressure generated by the ongoing supply shock.

This backdrop - which may well get significantly worse before it gets better - is a stark reminder of the risks of the Gulf's reliance on oil production, refining and export infrastructure networks that are highly vulnerable to military assault. But it's not just production that has been hit: Gulf countries need a lot of oil and gas just to keep their own lights on.

Asset Impact's asset-level data paints a series of cautionary tales across a power sector still far too dependent on gas - and in some cases, actively planning more.

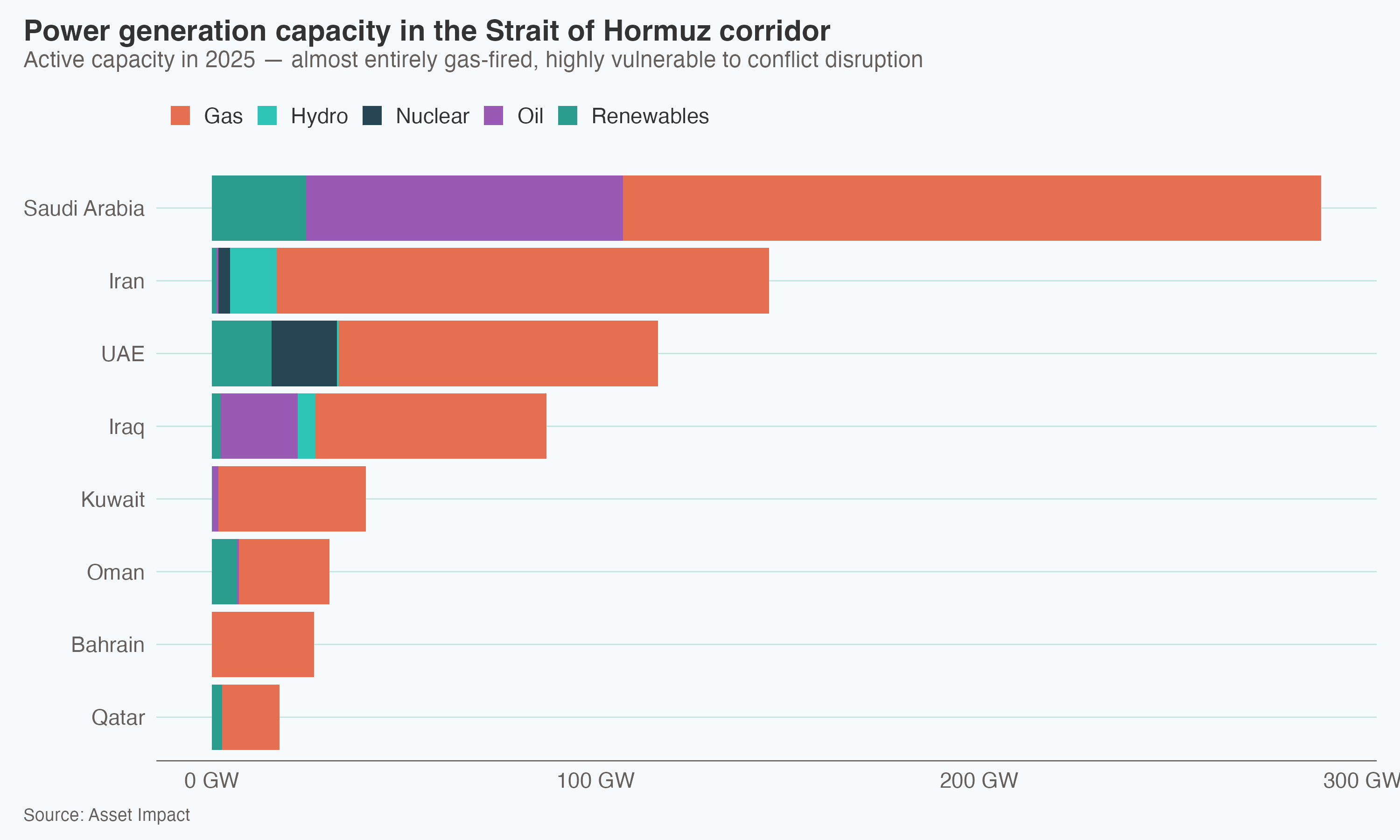

Power plants surrounding Hormuz are oil & gas-heavy

The Strait of Hormuz corridor, bordered by Iran, Iraq, Saudi Arabia, the UAE, Kuwait, Qatar, Bahrain and Oman, hosts ~290GW of gas-fired electricity generation capacity, and another ~40GW of oil-fired generators. Iran alone hosts 80GW of gas capacity.

Whether or not they are at risk of direct attack, these assets also require on reliable supplies of oil and gas. Keeping this capacity running just 70% of the time requires roughly 7.5 million barrels of oil every day.

Short-term memory losses: European utilities will suffer if war is prolonged

With 20% of global liquefied natural gas (LNG) transiting through the near-paralysed Hormuz corridor, continued ongoing disruption will cause global LNG spot prices to rise as Europe turns to US supplies and Asia competes with European buyers for Gulf supplies.

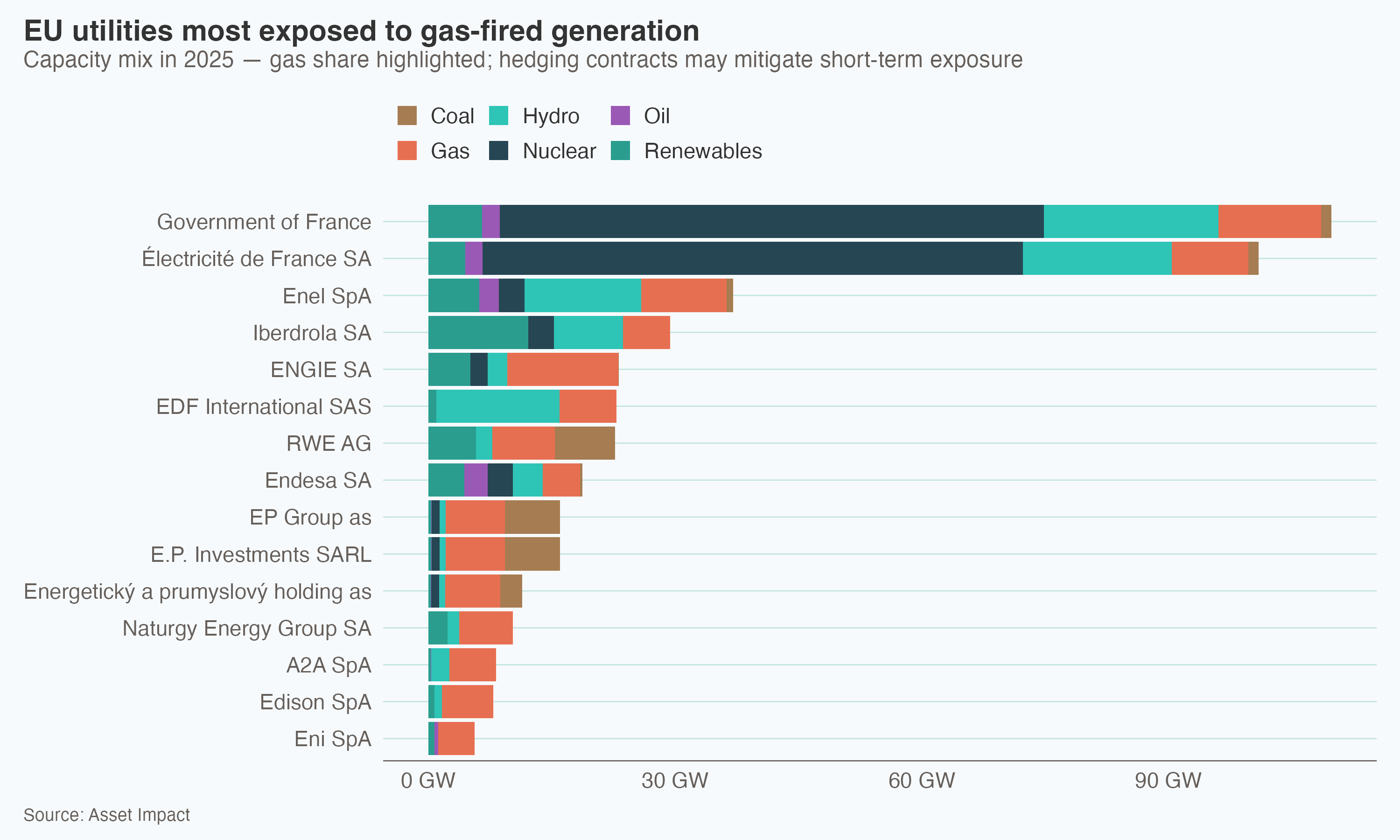

A chastening moment for European utilities and governments who, despite the massive, painful price shocks experienced in gas markets in 2022 and knock-on effects on both residential and industrial users - as well as taxpayer-funded price caps - following Russia's invasion of Ukraine, continue to promote gas-fired electricity generation as a transition fuel at home.

EDF, ENGIE, Enel, Endesa, RWE, EDP, Naturgy, Uniper and A2A, with their relatively large gas fleets, are all exposed. As the owner of EDF, so is the government of France. Most large utilities hedge gas procurement 1-2 years ahead. The prolongation of conflict in and around Hormuz, or a permanent rise in global LNG prices, would steadily exhaust these hedging protections and eventually expose utilities and their customers directly.

Gas: a dubious 'transition fuel' in more ways than one

Continued investment in long-lived fossil fuel infrastructure is usually promoted on the basis of energy security. Not only do these project lock in emissions for 20-30 years: they also lock in long-term exposure to fuel prices and geopolitical risks that are increasingly difficult and expensive to hedge. For Germany, which voluntarily retired the last dregs of its nuclear fleet in 2023, restricting its non-renewable supply options even further, the consequences are likely to be particularly severe. Europe's beleaguered heavy industry and households are likely to carry the cost of this dependency in the form of persistent energy price inflation and the knock-on effects on competitiveness and living standards respectively. With household finances already under pressure from inflation and unemployment stubbornly high, governments and financial institutions alike can benefit from anticipating price shocks using signals that asset-level data provides.

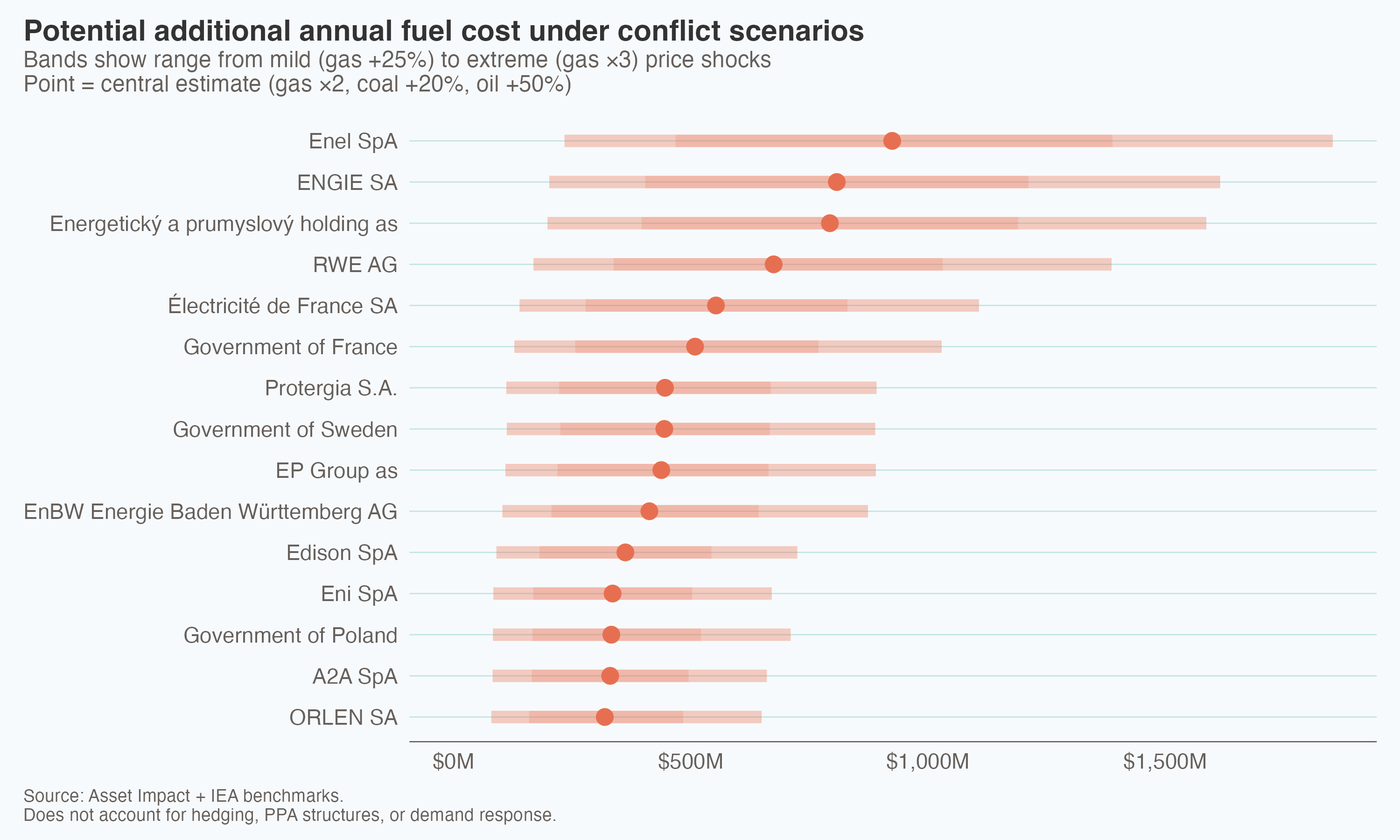

In a plausible drawn-out conflict scenario where gas prices double, oil prices stabilise at 50% higher than normal, and coal rises 20%, our forecasts find that the five most-affected European utilities face almost $3 billion in additional fuel costs as a result, overwhelmingly driven by gas. Through their ownership stakes in utility companies, the governments of France, Sweden and Poland are also exposed.

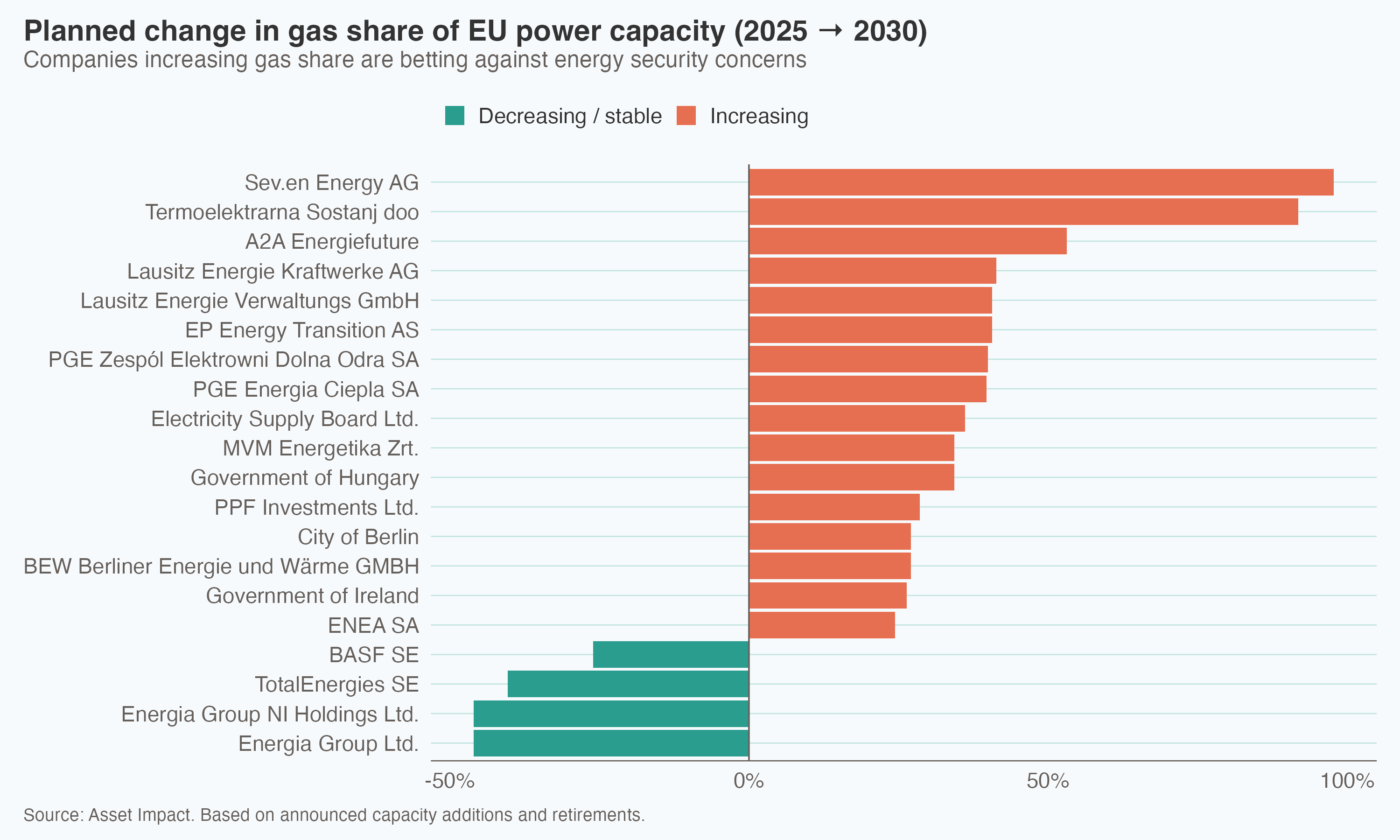

Despite the risks, Asset Impact's capex forecasts show that several large European utilities are becoming even more exposed to gas prices by 2030 by significantly increasing their dependency on combined-cycle gas capacity while retiring (relatively unaffected) coal plants. These include EnBW in Germany and PPC in Greece, as well as Czech conglomerate CEZ, which also operates across Germany, Hungary, Poland, Romania, Slovakia and Turkey. Our data shows that utilities in Germany alone are planning roughly 10GW of new gas capacity by 2031.

Renewable and nuclear power, of course, has effectively zero direct fuel price exposure. With many countries now able to partially rely on both forms of zero-carbon power as a cushion against war in the Gulf, 2026 is unlikely to be a like-for-like repeat of 1973. But the risks of domestic reliance on conflict-exposed supply chains and benefits of decarbonisation are obvious, almost independent of climate policy.

For Europe, the strategy of using gas as a transition fuel from coal is clearly backfiring for the second time in five years.

Let's talk

Looking for more details on using our forward-looking asset-based data? Our team is here to support you.

Contact us